Congress Overspends, but the Fed Inflates

By Alexander William Salter

Writing in The American Conservative, Rep. Josh Brecheen (R-OK) recently blamed inflation on irresponsible fiscal policy. He cites a barrage of statistics on the magnitude of the national debt, the looming insolvency of Social Security and Medicare, and the burdens high prices create for American households. Rep. Brecheen is partly right: perpetual deficits are bad for the economy, as well as for constitutional self-governance. But runaway deficits are not the primary cause of inflation. The Fed, not Congress, and the President is the chief culprit.

The connection between government spending and inflation seems obvious. Fiscal policy affects aggregate demand by changing total dollar-valued spending in the economy. If the government ratchets up spending, financed by borrowing, that should inject a new flow of funds into the national income stream. This is standard income-expenditure Keynesianism — and it’s wrong. We know this from history. Remember, the deficit increased significantly under Presidents Reagan and Obama. Inflation remained relatively static.

As Clark Warburton described it 80 years ago, deficit spending can increase dollar-valued national income only if it increases a) the rate of spending (velocity) for a given money supply or b) the money supply itself. Let’s consider each in turn.

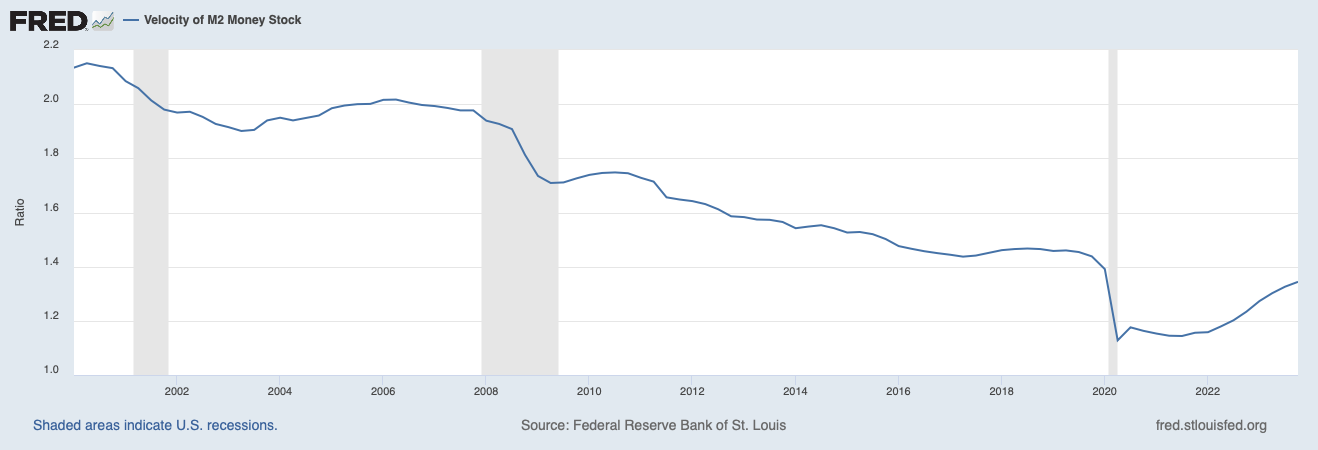

Deficits and Velocity

Deficit spending influences the rate of money turnover, which economists call the velocity of money. But its effects are small. Interest rates are the most probable mechanism. All else being equal, if governments are borrowing more to finance deficits, then demand for capital increases. That should push up interest rates. Higher rates, in turn, increase the opportunity cost of holding money. Hence we should see faster spending; velocity goes up.

Empirically, the increase in velocity following an increase in deficit spending appears to be small. It certainly does not explain the high inflation from late 2021 to early 2023. Velocity declined sharply amid the uncertainty of the first two quarters of 2020. Although it picked up in 2022, it remains below its Q4-2019 level.

Deficits and the Money Supply

The extent to which deficits increase the money supply, if at all, depends on how the buyers of government bonds finance their purchases. If it’s spent out of existing cash balances (either by households or businesses), the money supply doesn’t change. But if the banking system expands its liabilities to purchase the bonds, the money supply grows. This effect is noteworthy. As Warburton showed, the government’s overall fiscal stance had little power to explain dollar-valued national income, and hence inflation. But the money supply could. Even traditional fiscal operations have a monetary mechanism.

Much has changed since Warburton’s day, of course. Financial innovation destabilized the velocity of several common measures of the money supply, leading the economics profession to sour on monetarism. (But as economists such as Peter Ireland and Joshua Hendrickson have shown, velocity for the Divisia monetary aggregates, which weight money-supply components based on liquidity, remain quite stable and predictive of aggregate demand.) Monetary economists pay much more attention to interest rates. They shouldn’t; the money supply still matters most, especially when we consider Fed policy.

Everybody knows Washington spent an incredible amount of money during the COVID-19 response years. Everybody also knows the Fed massively increased its holdings of government bonds during the same period. In 2019, the deficit was just under $1 trillion; it ballooned to more than $3 trillion the next year. Over the same period, Fed holdings of Treasury debt rose from just over $2 trillion to nearly $4.75 trillion and peaked at just shy of $5.75 trillion in Summer 2022. As a result, the M2 money supply exploded from $15 trillion to almost $20 trillion at the end of 2020, reaching a maximum of $21.7 trillion in March 2022. As noted above, velocity declined over this interval, but only by about 15 percent. The money supply increase was roughly 40 percent. Consequently, inflation was higher than it had been for a generation.

At most, large deficits impelled the Fed to support the market for government debt by purchasing more debt than it should have. The central bank, not the fiscal authorities, is the residual determiner of aggregate demand. We can quibble with certain details — for example, Warburton’s Fed adhered to a pseudo-gold standard whereas ours is pure fiat — but the basic relationship between money, dollar-valued national spending, and inflation remains the same as in Warburton’s days.

Deficits are bad for the economy because they transfer resources from the productive private sector to the unproductive public sector. Deficits are bad for self-governance because they transgress a basic small-r republican commitment: not to saddle future generations with crippling debt before they are even old enough to vote. Rep. Brecheen is absolutely right to rail against fiscal follies. But he has the wrong target in his crosshairs if he’s concerned about inflation. Rather than pile on the feckless Biden administration, whose economic incompetence voters already know, he should raise public awareness about the Fed’s monetary mischief and work hard to bring the rule of law to monetary policy.

*****

This article was published by AIER, The American Institute for Economic Research, and is reproduced with permission.

TAKE ACTION

The Prickly Pear’s TAKE ACTION focus this year is to help achieve a winning 2024 national and state November 5th election with the removal of the Biden/Obama leftist executive branch disaster, win one U.S. Senate seat, maintain and win strong majorities in all Arizona state offices on the ballot and to insure that unrestricted abortion is not constitutionally embedded in our laws and culture.

Please click the TAKE ACTION link to learn to do’s and don’ts for voting in 2024. Our state and national elections are at great risk from the very aggressive and radical leftist Democrat operatives with documented rigging, mail-in voter fraud and illegals voting across the country (yes, with illegals voting across the country) in the last several election cycles.

Read Part 1 and Part 2 of The Prickly Pear essays entitled How NOT to Vote in the November 5, 2024 Election in Arizona to be well informed of the above issues and to vote in a way to ensure the most likely chance your vote will be counted and counted as you intend.

Please click the following link to learn more.

This article is courtesy of ThePricklyPear.org, an online voice for citizen journalists to express the principles of limited government and personal liberty to the public, to policy makers, and to political activists. Please visit ThePricklyPear.org for more great content.