Fed’s Lowest Lowball Inflation Measure Hits Another 30-Year High as Reckless Money-Printing Continues

By Wolf Richter

While the Fed is still printing $120 billion a month and repressing short-term rates to near 0% in the most monstrously overstimulated economy.

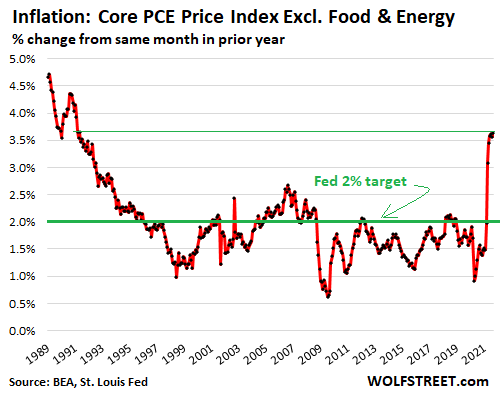

The lowest lowball inflation measure that the US government releases, the PCE price index without food and energy rose by 3.64% in September, compared to a year ago, the hottest inflation reading since May 1991.

This “core PCE” is the inflation measure that the Fed uses for its official inflation target of a “symmetrical” 2%. The reason it uses this measure is because it is the lowest lowball inflation measure the government publishes, and it understates actual inflation even more than other indices the government publishes. For example, CPI-U inflation in September was 5.4% and CPI-W was 5.9%, which themselves understate actual inflation.

Food and energy, precisely what regular people spend a lot of their money on, are excluded from the Fed’s inflation measure because prices of food and energy jump up and down a lot and create even more volatility in the inflation index.

But the regular headline PCE price index – we’ll get to it in a moment – has been running higher over the years than core PCE. Since 2012, when both index values were set to 100, the headline PCE index increased 1.5% faster than core PCE index.

The close-up of core PCE, covering the past 10 years, shows a little more closely what is happening on a year-over-year basis.

On a month-to-month basis, the core PCE index rose 0.21%, according to the Bureau of Economic Analysis today. Month-to-month readings are volatile. But when they’re bunched together in a long-term view, the dynamics emerge. Note the volatility in the 1970s, as inflation was rising, leading to year-over-year core PCE to exceed 10% in early 1975 and 9% in 1980. In between there were years paved with false hopes that this thing would go away on its own, but it didn’t, and interest rates were far higher already, and the Fed wasn’t doing QE:

*****

Continue reading this article, published October 29, 2021 at Wolf Street.

This article is courtesy of ThePricklyPear.org, an online voice for citizen journalists to express the principles of limited government and personal liberty to the public, to policy makers, and to political activists. Please visit ThePricklyPear.org for more great content.