The Inherent Contradictions of Socialism

By Neland Nobel

Forecasting the economy is always difficult, but the number of external and internal variables associated with this business cycle is unusually complex. Forces of recovery from lockdown and gigantic fiscal and monetary stimulation are colliding with record-high debt, overvaluation in many markets, and severe inflationary pressures that must be dealt with. If that is not enough, now we get to mix in war and a serious oil and food price shock.

The odds of recession seem to be growing. We will be very lucky if we can avoid one.

Among the difficulties are the government’s astounding mistakes concerning the Covid policy. While some latitude must be given to the novel nature of the Coronavirus, the government went overboard and basically shut down production with its “stay at home orders” and other restrictions, while at the same time bulling up demand by running huge deficits and handing out money to the public. That decrease in supply and increase in demand is partially responsible for record-high deficits and price inflation.

Apparently, our leaders thought something as complex as the international economy could be turned on and off like a light switch. It obviously has proved to be much more complex than that.

There has never been a response to a pandemic before like this in American history. Rather than taking their playbook from previous experiences in America such as the Spanish flu or polio, government agencies seemed more favorable to the Communist Chinese model. Subsequent studies by Johns Hopkins showed that economic disruption bought by “lockdown” policies did very little in terms of improved health outcomes.

Another government agency, the Federal Reserve Board which feigns independence, deliberately advertised its desire to increase inflation, kept interest rates too low for too long, and kept injecting reserves into the banking system through continual “quantitative easing.” Never in centuries of financial history have interest rates been kept so low, for so long.

This combination of excessive monetary and fiscal policy created massive inflation first in asset prices. It has pushed stocks, bonds, and real estate into record territory. There is significant evidence that the Federal Reserve deliberately set about to elevate asset prices, claiming that a “wealth effect” would prove positive for the economy.

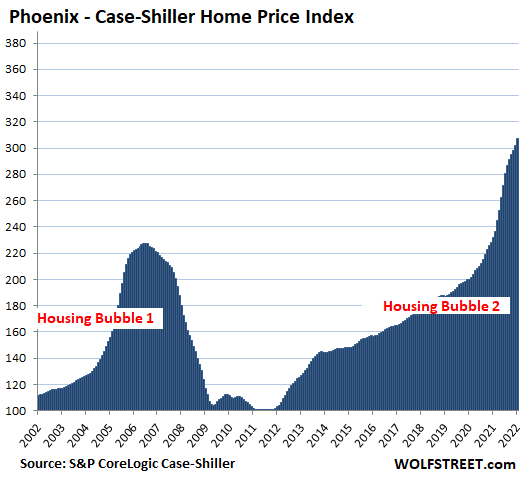

But the wealth effect largely benefited the ultra-wealthy that owned assets and makes large donations to political parties. For working people, homes are now too expensive for many to purchase, and even rent for apartments in most major cities now exceeds the normal rule of thumb of not exceeding one-third of income. Housing costs are squeezing the middle class.

Equity prices too have become quite elevated. The Cyclically Adjusted Price to Earnings ratio (the so-called CAPE ratio) is just one measure among many that indicates high equity prices. The average CAPE ratio for example over the past 10 years is about 17, while the market at the most recent peak was above 37. This would require a drop of more than 50% just to return to the mean average. And during bear markets, there is always a tendency to overshoot to the downside.

Markets that have been elevated by ultra-loose monetary and fiscal policy, tend to weaken and create a “reverse wealth effect” when they decline. While timing such moves is extremely difficult, it would seem reasonable that markets that have been stimulated to high levels by cheap money run the risk of retreating when then cheap money policies are reversed.

With Republicans likely to take the mid-term elections, fiscal policy will hopefully become saner, and Federal spending decline. And the Federal Reserve has vowed to fight the inflation they helped set loose on the country by raising interest rates. So, it would seem easy money policies will be reversed, at least for a while.

Higher rates mean lower bond prices and we are just completing the worst quarter on record for the bond market. Bonds are already in a bear market and even with this decline, bonds have a yield well below the rate of price inflation.

Equity markets have held up better. True, some smaller cap indices and foreign markets have fallen more than 20%, but the large-cap indices have not, and hence have had a “correction”, but nothing yet too traumatizing.

Thrown into this mix we must add very high energy costs. It is just not their nominal level; it is the record speed prices rose to these levels. This is taking money away from other purchases. Compounding that problem is the Biden Administration has openly declared war on American energy producers, all the while begging for more oil from dictators and enemies in Venezuela and Iran.

While Putin built up for months his army on the border of Ukraine, the West seemed quite surprised when the invasion took place. Europe seemed astounded to learn their “green” policies left them hostage to a thug like Putin.

But along came another surprise. Both Ukraine and Russia produce a lot of food, especially grain, and the invasion clearly will disrupt both trade in food and the normal planting season.

The spike in energy hits food producers outside of the conflict area. American farmers are reporting difficulties with record-high fertilizer costs, energy costs, and equipment shortages due to continued supply chain and labor issues. This will be equally true of farmers in Argentina, Brazil, Canada, and Australia.

Food prices will put added pressure on hard-pressed consumers and likely will create social and political turmoil in poorer regions of the world. Once again, it is not just the high prices, it is the speed that prices got to this level. Such rapid moves tend to shock the consumer and hence the economy since consumer spending is 70% of GDP. Such rapid increases in food and fuel are beyond the capacity of most individuals or corporations to adapt.

While economies do have a cyclical nature (that is why it is called the business cycle), this particular cycle seems to have an abnormal amount of government interference written into it.

Just in the last two years, it was the government that shut down the economy, touched off inflation, held interest rates too low for too long, paid people not to work, and disrupted the labor markets.

It is the government that goes to war and it is government policy that is restricting the supply of energy due to their policy of a Green New Deal.

Record high housing costs, high fuel costs, high food costs, and overall inflation coupled with supply chain problems. All brought to you by your government!

All of these factors come together at a time when markets are abnormally elevated in price, and both government and private sectors are carrying huge amounts of debt.

Perhaps the Federal Reserve can raise rates high enough to kill off inflation, without harming the economy too much. This is the much-desired “soft landing.”

But that was argued before in the last two cycles (2000-2002) and (2007-2009) and the goal remained elusive. Particularly the last recession had the dangerous effect of creating a housing crisis, which in turn created a banking crisis, which lead to record bailouts of financial institutions and unprecedented monetary policy which remained in place far past the emergency period.

One of the most reliable indicators of recession has been the “inversion of the yield curve.” Normally, the longer you contract for money, the higher the interest rate. That only makes sense, since over time more bad things can happen such as default and inflation. Higher risk should create a higher interest rate. That would be a normal shape for the yield curve, i.e., longer rates are higher than shorter rates. But when short-term paper carries an interest rate higher than long-term paper, you have a major distortion in the credit markets.

In the chart above, when inversion occurs, the chart goes to zero or below. Notice inversions lead by a year or so, the onset of a recession, the gray vertical bar. The chart is interactive so you can peruse the last 40 years of history.

Very recently, the yield on short paper, the two-year Treasury bond, is about the same as it is on 10-year bonds. If short rates move above longer rates, this is the inversion of the yield curve. Such inversions have had an almost flawless record of preceding recessions.

There are some other indicators as well we can briefly touch on. The rate of change of money supply growth is starting to fall, consumer sentiment looks wobbly, real incomes have been falling for seven months, and Biden plans a massive tax increase. All these are negatives for the economy.

The probabilities grow not just for a slowdown, but a slow down with persistent price inflation. This is the dreaded “stagflation” of the miserable years of Jimmy Carter.

If indeed we do nose into recession, we hope citizens will remember all the governmental factors involved in this particular business cycle. This one the Left can’t blame on the “inherent contradictions” of capitalism.

Almost all of the factors mentioned stem from the failure of government policy or are the consequence of government manipulation and intervention which distorted values, debt levels, and market forces.

No, this recession will be caused by the inherent contradictions of socialist intervention.

This article is courtesy of ThePricklyPear.org, an online voice for citizen journalists to express the principles of limited government and personal liberty to the public, to policy makers, and to political activists. Please visit ThePricklyPear.org for more great content.